Inheritance Tax (IHT) Explained

In this guide, you’ll learn how it works, how Inheritance Tax is calculated, who must pay it, and what to do if you can’t afford it.

Inheritance Tax: A Complete UK Guide

Inheritance Tax, or IHT, is the tax charged on the value of a deceased person’s estate. Tax is charged at 40% on the portion of the estate above the Inheritance Tax threshold. IHT can be complicated, but this guide explains how it works, how it is calculated, who must pay it, and what to do if you can’t afford it.

How much is Inheritance Tax?

The single person’s Inheritance Tax threshold in the UK is £325,000. Tax must be paid when the value of an estate exceeds this amount, at a rate of 40% on the excess.

| Estate value | £500,000 |

| Minus nil-rate band | − £325,000 |

| Taxable amount | £175,000 |

| IHT at 40% | £70,000 |

In the 2019/2020 tax year the average Inheritance Tax bill was over £220,000, an increase on previous years. These rates apply to a single person’s allowance; different rules apply for married couples and those in civil partnerships.

Who pays Inheritance Tax?

If there is a Will, the Executor is usually liable to settle the Inheritance Tax bill. If no Will has been left, the responsibility falls to the Administrator (Personal Representative) of the estate. Once IHT has been settled, the Executor or Administrator can apply for a Grant of Probate and distribute the estate to beneficiaries.

Probate and Inheritance Tax

The Executor or Administrator must obtain a Grant of Probate in order to dispose of estate assets, and this cannot be issued until the IHT has been paid to HMRC. Probate is the legal right to deal with the deceased person’s property, money, and possessions. In Scotland this is known as Confirmation.

Certain estates are exempt — including those of people who die while on active service (armed forces, police, and paramedics). This exemption also applies if a person is injured on active service and their death is hastened by the injury, even if they had since left active service.

Does a spouse pay Inheritance Tax?

Married or registered civil partners do not pay any Inheritance Tax on assets left by their spouse. When the second partner dies, the estate qualifies for a married couple’s Transferable Nil Rate Band (TNRB) — the sum of two individual allowances, totalling £650,000 (provided none of the IHT threshold was previously used). The person inheriting this estate only pays tax on anything over £650,000.

Do cohabiting couples have to pay Inheritance Tax?

There is no specific Inheritance Tax allowance or exemption for cohabiting couples. If you are not married but own assets jointly, the situation can become complex — particularly where property is concerned.

If you are joint tenants (meaning you both own all of the property) and your partner left you everything in their Will, you would face a 40% tax bill if the total assets (including property) exceed the single person’s £325,000 threshold. Without a Will, the property may still transfer to you via the right of survivorship, but family members of your partner would have a legal claim on other assets. In that scenario, the administrators become responsible for paying the tax bill.

When do you pay Inheritance Tax?

Inheritance Tax must be paid before Probate can be granted and before assets are distributed. The bill must be settled within six months of the person’s death. After this deadline, HMRC begins charging interest — currently at 3.75% — on the unpaid amount, and may add penalties. HMRC will refund the estate if it has overpaid IHT once Probate has been granted.

What do you pay Inheritance Tax on?

IHT is calculated on the net value of the estate — that is, total assets minus any outstanding debts. Assets included are: bank accounts, pensions, properties, jewellery, vehicles, shares, jointly owned assets, and insurance policy pay-outs. Debts that reduce the taxable value include mortgages, funeral expenses, and other taxes or estate management costs.

| Gross estate value | £600,000 |

| Minus mortgage remaining | − £150,000 |

| Minus funeral expenses | − £10,000 |

| Net estate value | £440,000 |

| Minus nil-rate band | − £325,000 |

| Taxable amount | £115,000 |

| IHT at 40% | £46,000 |

Do you pay Inheritance Tax on a house?

Whether IHT is due on a property depends on its value and who inherits it. If the deceased’s primary residence is left to direct descendants (children or grandchildren), they can access an additional tax-free allowance — the Residence Nil Rate Band (RNRB) — of up to £175,000 per person, on top of the standard £325,000 threshold. This means up to £500,000 per individual may be free of Inheritance Tax.

Where the estate passes to a surviving spouse and then to direct descendants, it is possible to have up to £1 million in combined tax-free allowance (£325,000 × 2 nil-rate bands + £175,000 × 2 RNRB). The £175,000 RNRB only applies where the estate is worth under £2 million; above that, the allowance tapers by £1 for every £2 over the £2 million threshold.

If the property passes to beneficiaries who are not direct descendants, the standard 40% rate applies to anything over the £325,000 allowance.

Do you pay Inheritance Tax on gifted money?

You do not pay tax on cash gifts during a person’s lifetime, but strict rules apply. Gifts made while someone is alive are known as potentially exempt transfers (PETs). If the donor lives for more than seven years after making the gift, it is fully exempt from IHT. If they die sooner, a sliding scale of tax applies — known as taper relief:

| Years between gift and death | IHT rate on gift |

|---|---|

| Less than 3 years | 40% |

| 3 to 4 years | 32% |

| 4 to 5 years | 24% |

| 5 to 6 years | 16% |

| 6 to 7 years | 8% |

| More than 7 years | 0% |

Gift values are assessed at the time of donation, and gifts use up the nil-rate band before other assets such as property are calculated.

Are there any gifts exempt from Inheritance Tax?

The following gifts are exempt from IHT:

- Gifts to your spouse or civil partner

- Gifts to charities

- Multiple gifts up to £250 per year to any one individual

- Payments to help an elderly relative or minor with living costs

- Gifts totalling £3,000 or less in any tax year (excluding the £250 gifts above, provided they are not to the same person)

- Gifts made seven years or more before the giver’s death

When a couple marries, people may also give the following wedding gifts free of IHT:

- Parents: up to £5,000

- Grandparents: up to £2,500 each

How to pay Inheritance Tax

There are a few ways to make an IHT payment, and any overpayment can be reclaimed from the estate once Probate has been granted.

How to pay Inheritance Tax before Probate

An Executor or Administrator can pay IHT from their own bank account using the IHT reference number — online, via telephone banking, CHAPS, BACS, or at a bank. Payment can also be made from any joint accounts held with the deceased.

How long does HMRC take to process Inheritance Tax?

Before applying for Probate, you must send form IHT400 and form IHT421 to HMRC and wait 20 working days. You will usually need to pay some or all of the IHT before Probate is granted — though if paid from your own account, this can be reclaimed from the estate afterwards.

What happens if you can’t afford to pay Inheritance Tax?

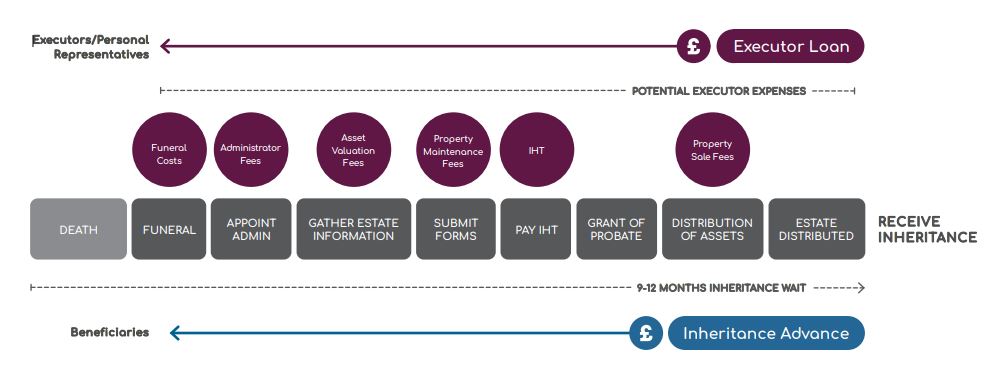

Many estates are asset-rich but cash-poor. Because IHT must be paid within six months of death, this creates a difficult situation: the Executor needs a Grant of Probate before they can sell estate assets to raise the money — but the Grant cannot be issued until IHT is paid.

Where assets such as property may take longer to sell, HMRC allows IHT to be paid in annual instalments over 10 years, with the first instalment due six months after the death. Interest is charged only on late instalments. Once the assets are sold, any outstanding balance must be repaid in full.

How to get a loan to pay Inheritance Tax from Level

Regulated by the Financial Conduct Authority, the Level IHT Loan is paid directly to HMRC, allowing families to start the Probate process and receive their inheritance. Apply today or call our team on 0207 205 2870. We also offer an award-winning Inheritance Advance for beneficiaries who want to access their inheritance sooner.

Interested in applying for funding?

Apply now using the button below. A member of the team will review your information and arrange a time to speak with you.

Apply for funding today